External data minimized

Created new rating modifier

Changes to group policy pricing

Enhanced pricing accuracy

The challenge

Enhancing claims prediction and pricing accuracy

The health insurer sought to enhance its ability to predict claims experiences by integrating external data with its internal claims data. The primary goal was to improve pricing for new business by incorporating external factors, in addition to traditional variables like age, gender, and region, to create more accurate and informed pricing models.

Key challenges

Integrating external data with existing internal systems

Effectively leveraging external data to create accurate and reliable pricing models

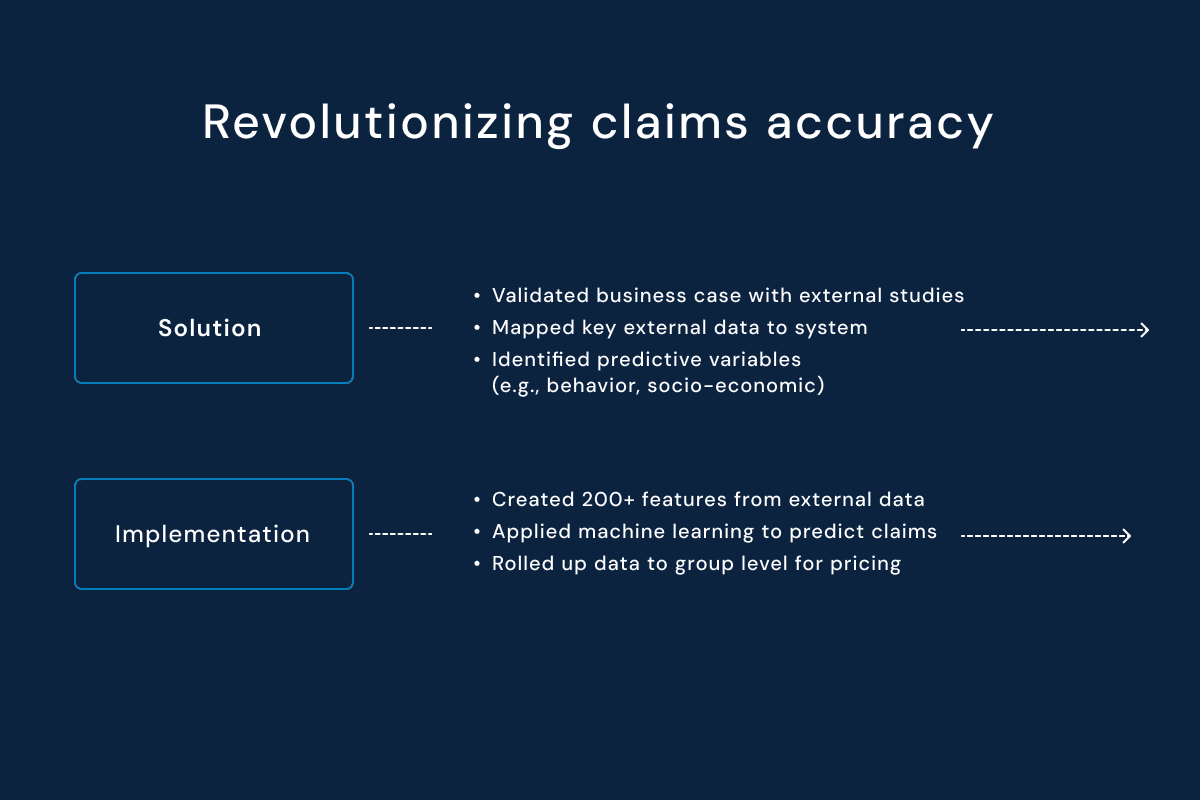

The solution

Optimizing claims prediction with machine learning

External data integration

Integrated external data for predictions

Used behavior and socio-economic indicators

Created a rating modifier to refine risk

Enhanced claims prediction

Used ML to predict claims

Identified key drivers (e.g., TV usage)

Reduced loss prediction gap

Implementation approach

1

Discovery phase

Validated business case

Identified key variables

Mapped external data

2

Model development

Created 200+ features

Used ML for prediction

Rolled up data for pricing

3

Results

Developed rating modifier

Reduced prediction gap

Improved pricing accuracy

The impact

Enhancing risk prediction for smarter pricing

Improved risk prediction

Closed claims prediction gap

Improved loss accuracy

Strengthened pricing

Optimized pricing

Integrated rating modifier into pricing

Adjusted quotation process

Aligned premiums with risk

Data-driven decisions

Improved claims prediction with external data

Strengthened underwriting framework

Informed pricing adjustments

Looking ahead

Expand data sources

Incorporate additional external variables for more precise predictions

Refine pricing models

Continuously adjust group policy pricing for improved accuracy

Enhance underwriting process

Leverage predictive analytics for more effective risk management